Major Economies Developing CBDCs To Revolutionize Payments

I90% of central banks are investigating CBDCs, including 19 of the G-20 countries and the European Union block.

114 countries, representing over 95 per cent of global GDP, are exploring a CBDC (Central Bank Digital Currency). Among these, 16 from the G-20 countries are already in the development or pilot stage of CBDC implementation. China has a significant first-mover advantage with its e-CNY, which is anticipated to become the first CBDC issued by a major economy.

All the major economies developing CBDCs are primarily focusing on wholesale CBDCs (that can revolutionize payments related to trade, investment, and high-value settlement, driven by the aim of challenging the worldwide dominance of the US dollar in the long term.

And India is no different. The Reserve Bank of India (RBI) has been actively developing its pilot program for the digital rupee or e-Rupee and has created a stir amongst fintech enthusiasts. The recent signing of the MoU with the Central Bank of UAE to explore the interoperability between the CBDCs of CBUAE and RBI suggests that India is taking a step towards enhancing the global recognition of the Indian rupee.

Given these developments, our blog aims to delve into the intricacies of the Reserve Bank of India’s latest digital currency pilot and its potential ramifications on India’s digital payments industry as well as the global economy.

So, let’s understand some of the basics.

What exactly is the e-Rupee, you ask?

Well, in simple terms, it’s digital money!

The e-Rupee is a tokenized digital version of the Indian Rupee that will be issued by the RBI (in the same denominations as paper currency and coins) as a central bank digital currency (CBDC) and loaded into a digital wallet.

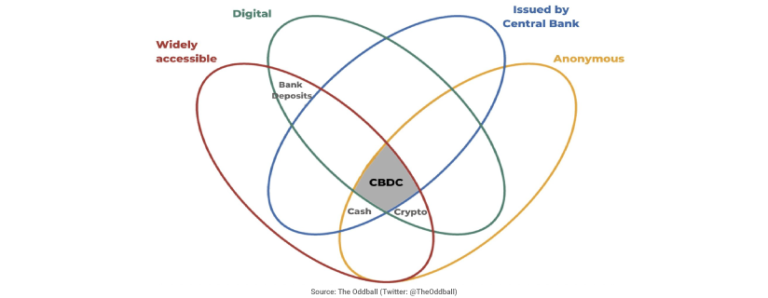

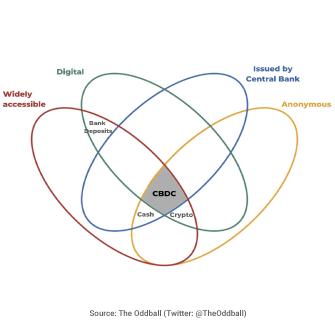

This innovative solution offers the best of all worlds, combining the anonymity and digital features of cryptocurrencies, the regulatory oversight of cash, and the widespread accessibility, speed, and cost efficiency of UPI.

There are two types of CBDCs that make up the digital version of the e-Rupee.

1. Wholesale Digital Rupee, aka e-Rupee-W, which is used for trade between the central bank and public/private banks. This account-based digital currency eliminates liquidity and counterparty credit risks that can slow down financial systems.

2. Retail Digital Rupee, aka e-Rupee-R, a token-based digital version of the fiat currency used by the public for day-to-day transactions.

So does India really need an e-Rupee? It looks like now would be as good a time as any!

Printing and managing cash in India cost around $600 million, and cash in circulation accounts for 14% of the country’s $3.18 trillion GDP.

In India, most citizens prefer to use cash for their daily transactions. Surprisingly, physical cash usage increased 72% after demonetization in 2016! However, post the pandemic, the popularity of digital payments substantially increased, returning to former levels and even surpassing them in several cities. According to Visa, India may save a stunning $56 billion by moving more transactions online by 2025.

A digital payment system that can be used anytime, anywhere – even without access to bank accounts. That’s where the e-Rupee brings transformation: with its ground-breaking capability of transferring money even in remote areas and beyond traditional banking channels!

But wait, aren’t instant payment rails like the UPI doing the same job?

UPI and e-Rupee may appear to do the same job, but there are distinct differences between them. While UPI is a payment system, e-Rupee is legal tender.

When it comes to transferring money via UPI, banks must be involved in order for a clearing and settlement process to take place – only then will funds reach the destinations. In contrast, with the e-Rupee, you can make digital payments without any help from intermediary parties or your bank; transactions occur almost instantly with anonymity so that both sender and receiver know they have exchanged value securely right away.

However, the current pilot version of the e-Rupee, requires internet access and involves banking intermediaries for loading funds into the e-wallet, and may not fulfil the goal of achieving greater financial inclusion or the proposition of complete anonymity.

Fascinating Fact: Over 50% of India still hasn’t hopped on the UPI train. So there is ample room for the e-Rupee in the market.

Potential impact on the implementation of e-Rupee

When it comes to introducing CBDC in a growing market like India, the RBI has taken steps to manage any impacts on monetary policy.

RBI has set a cap on how much CBDC an individual can hold to prevent massive conversions of CASA accounts to CBDC holdings. This helps banks maintain liquidity and stay on top of things. Also, with zero interest offered on e-Rupee wallets, the potential for arbitrage between bank deposits and CBDC is minimized.

From a corporate treasury perspective, the introduction of the e-Rupee may require some adjustments. Since CBDC wallets do not typically offer overdrafts, corporate treasurers will need to ensure that their wallets are funded before initiating payment transactions. As CBDCs do not carry interest, corporate treasurers may need to convert their end-of-day CBDC positions into regular interest-bearing currency to effectively manage their balance sheets.

Another key impact is on the existing payment rails. Since CBDC’s work on DLT (Distributed Ledger Technology) and existing payments infrastructure doesn’t support the same, it is imperative that the e-Rupee be integrated with existing payment systems like UPI, digital wallets, etc. because interoperability between payment systems contributes to achieving adoption, co-existence, innovation, and efficiency for end users.

Game-Changing Propositions

One use case that RBI is yet to talk about is Programmable Payments (Think Direct Benefit Transfer – DBT). With this system in place, citizens can access central bank money that has been programmed for specific purposes like LPG subsidies or fertilizer support. Furthermore, these “programmed e-Rupee ” must be redeemed at authorized banks and outlets to ensure they are not misused; after which recipients have the flexibility to convert them back into regular e-Rupee or physical cash.

Another potential use case could be in Cross Border Remittances. As per a World Bank report, India received remittances worth $100 billion in 2022, making it the top recipient of such transfers globally. Currently, international money transfers require intermediaries (correspondent banks), resulting in high transaction fees and long processing times. e-Rupee remittances could happen in real-time, slashing the time it takes for the intended recipient to receive their payment as the money flows from the digital wallet of the remitter to the digital wallet of the beneficiary seamlessly and directly between the two central bank digital currencies based on the agreed FX rate and protocol. Of course today cross holdings in CBDC’s are not yet possible ( central bank of country X cannot hold CBDC of country Y ) but once this mechanism is established and matures, cross border remittances using CBDC will become an obvious use case. This is already in pilot by SWIFT, BIS and a consortium of banks.

Facilitating secure offline payments can also be a notable benefit of CBDCs, particularly for the approximately 575 million individuals in India who lack internet connectivity. However, offline processing modes of CBDC are still in evolution and involve multiple considerations such as prevention of double spending, loss of device, reconciliation with the central ledger once online, etc.

Insights from the First Few Months of the Pilot Program

So it looks like the e-Rupee-R (retail) hasn’t really caught on with consumers and merchants despite being launched five months ago. While CBDCs can offer a range of benefits like promoting financial inclusion and boosting payment system efficiency, competition, security, and resiliency, an IMF paper suggests that the UPI’s existence might make it less appealing for users to adopt the e-Rupee in India.

However, the newly launched e-Rupee -W (wholesale) system has seen impressive results in its pilot phase, with daily trades of government securities recording up to INR 2 billion. This platform eliminates the need for any settlement guarantee infrastructure, reducing the counter-party risk and providing more efficient settlements at a fast pace. Albeit, with CBDC transactions being settled instantly, banks can no longer enjoy the intraday liquidity that they had when they settled on a netted T+1 basis. This means that banks need to manage their intraday liquidity more actively.

Conclusion:

The RBI’s e-Rupee innovation is primed to revolutionize India’s financial landscape by offering a secure and efficient digital payment system with programmable features, and while wholesale CBDC may become crucial for cross-border payments, leaving the benefits of retail CBDC up for debate.

This crucial first step towards the future of Indian digital payments may take some time to reach widespread adoption – but that doesn’t stop us from imagining how far it can go! So join in on the journey as we stay tuned for what promises to be an exciting development ahead.

Perspectives

How SWIFT gpi is transforming Cross-Border Payments

Intellect Global Transaction Banking (iGTB) identified as a leader and "Best in Class" Payments Platform provider

Payments fund control – Realtime limit management while doing Fund transfer for your corporate customers