News Flash

Africa Roundtable Event

Learn More News FlashiGTB Pulse Newsletter May 2025

Learn More News FlashHighlights of iGTB at EBAday 2025

Learn More News FlashEnhancing Corporate Payment Efficiency with SWIFT GPI Tracker powered by eMACH.ai

Learn More News FlashEmpower Digital Payments: KPI-Driven Payments with Self-Service Intelligence

Read More News FlashUnlocking Africa’s Trade Finance Potential: Driving Growth Through Digital Innovation

Read More

Contextual Banking Experience (CBX)

To help corporate and SME clients originate payments on a rich contextual omni-channel platform

Payments Service Hub

Bulking, Debulking, Validation, Enrichment, Orchestration and PSR generation

ISO 20022 Remittance Data Management

That helps banks create a remittance repository and monetize the investment in iso20022

Contextual Payments Engine

Based on rules to give recommendations of cheapest and fastest rails and other AI/ML based recommendations for upsell and cross sell

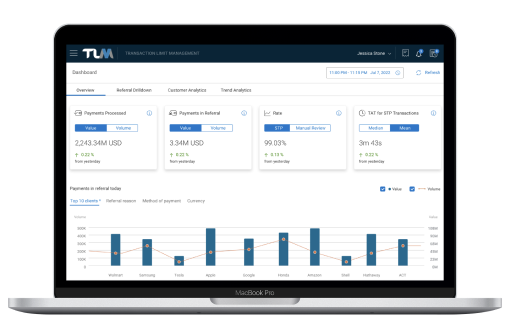

Transaction Limits Management

Real time payments exposure control across complex client account structures helping banks minimizes risk

Virtual Accounts and Liquidity Management

Pre-integrated with the payment's platform for a holistic digital transaction banking experience, to help banks offer POBO, COBO, receivables reconciliation, and other VAS

FedNow Payments

Transaction Limits Management

FedNow Payments

Unlock Real-Time Banking with iGTB’s FedNow Payment Solutions

Empowering Financial Institutions across the USA with 24/7/365 Instant Payments. Explore our innovative solutions, tailor-made for your bank’s business customers.

Learn MoreTransaction Limits Management

Real-time risk and limits management solution to optimize corporate liquidity and working capital

iGTB designed Transaction Limits Management (TLM), a system that processes corporate payments by checking client balances and limits in real-time and gives a pay/ no-pay/refer decision based on corporate cash and liquidity structures and shared limits thereby reducing limit breach risks while improving client experience and STP.

Client Testimonials

Explore testimonials showcasing how iGTB empowers 60% of the world’s top banks to #winwitheMACH.ai

CIBC Is focused on innovation that makes a difference for our clients and leveraging IGTB's payments platform enhances our ability to deliver new capabilities, support emerging technologies such as blockchain, and positions us well to lead in the rapidly evolving payments market in Canada and the United States as they move towards real time payments

Phil Griffiths

SVP & Head of

Global Transaction Banking

Global Transaction Banking

CIBC Is focused on innovation that makes a difference for our clients and leveraging IGTB's payments platform enhances our ability to deliver new capabilities, support emerging technologies such as blockchain, and positions us well to lead in the rapidly evolving payments market in Canada and the United States as they move towards real time payments

Phil Griffiths

SVP & Head of

Global Transaction Banking

Global Transaction Banking

Microservices Architecture

Loosely coupled, self contained services

API First

Build internal ecosystems with open APIs

100 % Cloud Native

Flexibility to deploy on any public cloud platforms

Pluggable Backends

Integrate any backend or application gracefully with pluggable integrations

Security

With layers of security, ready for public or private cloud deployment

No Vendor Lock In

Usage of open source components based on CNCF

Microservices Architecture

Loosely coupled, self contained services

API First

Build internal ecosystems with open APIs

100 % Cloud Native

Flexibility to deploy on any public cloud platforms

Pluggable Backends

Integrate any backend or application gracefully with pluggable integrations

Security

With layers of security, ready for public or private cloud deployment

No Vendor Lock In

Usage of open source components based on CNCF

Microservices Architecture

Loosely coupled, self contained services

API First

Build internal ecosystems with open APIs

100 % Cloud Native

Flexibility to deploy on any public cloud platforms

Pluggable Backends

Integrate any backend or application gracefully with pluggable integrations

Security

With layers of security, ready for public or private cloud deployment

No Vendor Lock In

Usage of open source components based on CNCF